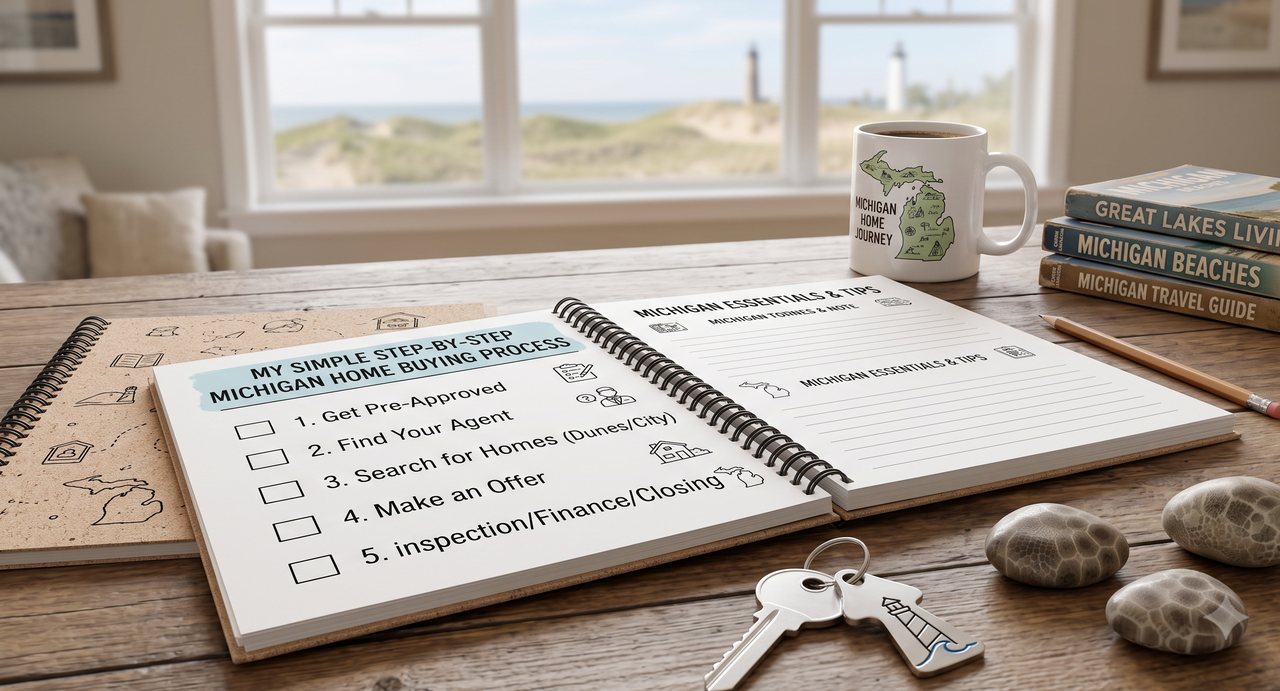

Most people who feel overwhelmed by buying a home are not overwhelmed by the home. They are overwhelmed by not knowing the order of operations. They worry they will tour a house, fall for it, and then learn they skipped a step that loses the deal. The good news is that buying a home in Michigan follows the same path almost every time, and once you can see that path laid out, the fear goes away. Here is how it actually works, start to finish, with the West Michigan details that tend to surprise people.

Start with the money, not the listings

It feels backward, but the first move is a conversation with a lender, not a Saturday of open houses. A lender reviews your income, credit, and debts, and tells you what you can actually borrow. That conversation produces a pre-approval letter, and that letter is what turns you from a browser into a buyer. Without it, sellers in a competitive market often will not take your offer seriously, and you risk falling for a home a tier above what you can finance.

A word on the distinction here: a lender quotes the numbers, not me. I can tell you how the process works and what a strong pre-approval looks like, but the rate, the payment, and the loan program are theirs to give you in writing. Talk to at least one local lender early, because those figures are the foundation everything else sits on.

Find a REALTOR(R) who actually knows your market

A good REALTOR(R) is not someone who unlocks doors. The door part is easy. The value is in what you cannot see from the listing photos: what a fair price looks like on this street, which inspection findings are normal for an older home versus a real problem, how to structure an offer that wins without overpaying, and how to keep a deal from quietly falling apart before closing. Pick someone who knows your target townships, listens more than they pitch, and tells you when a house is wrong for you.

House hunting, the productive way

This is the fun stage, and also where buyers waste the most energy. Your agent sets you up with alerts pulled straight from the MLS, so you see new listings as they hit rather than days later on a public site. Then you tour together and compare what matters beyond the kitchen: condition, location, school district, and the true cost to own.

That last point is where West Michigan trips people up. Two homes with the same price tag can carry very different monthly costs once you account for property taxes and heating. Taxes vary by township and city, and a home that has not sold in years can see its taxable value reset after you buy, which raises the bill. Older homes heated through a long Michigan winter often cost more to run than a newer, tighter build. None of this should scare you off a house. It should just shape how you compare them.

Making an offer

When you find the right one, your agent prepares a written offer. Price is only one part of it. The offer also names your earnest money deposit (a good-faith amount that shows you are serious and gets credited back at closing), your financing type, your proposed closing date, and your contingencies. Contingencies are the conditions that let you walk away without losing your deposit, most commonly an inspection contingency and a financing or appraisal contingency.

A strong offer is not always the highest one. It is the one structured to match what the seller wants, whether that is a clean close, a flexible date, or fewer conditions, while still protecting you. Reading that correctly is most of the job.

Inspection and appraisal

Once your offer is accepted, two independent checkpoints run, and they answer different questions. The home inspection is for you. A licensed inspector walks the property and reports on its condition, from the roof and furnace to the outlets, so you buy with eyes open. If something significant turns up, you can negotiate repairs or a credit, or in some cases walk away under your inspection contingency.

The appraisal is for the lender. An appraiser confirms the home is worth what you agreed to pay, because the bank will not lend more than the property is worth. If it comes in low, that gap has to be solved before closing, usually by renegotiating the price, bringing extra cash, or challenging the appraisal. Your agent steers both conversations.

Final approval and the road to closing

With the inspection and appraisal behind you, your file goes back to the lender for final underwriting. They re-verify your documents, confirm nothing major has changed (this is why you do not finance a car or open new credit cards mid-purchase), and clear the loan to close. Meanwhile a title company researches the property's history to confirm the seller can legally sell it and that no old liens follow you onto the title.

In Michigan, the stretch from accepted offer to keys in hand commonly runs around 30 to 45 days, though a cash purchase can move faster and a complicated file can run longer. Federal rules also require your lender to deliver a Closing Disclosure, the document with your final loan numbers, at least three business days before you sign, so you get real time to read it before signing day.

Closing day

Closing usually happens at the title company's office. You sign the paperwork, the lender funds the loan, the title company records the deed with the county, and the home becomes legally yours. Bring a government photo ID and any funds you owe by wire or cashier's check, and never trust last-minute wiring instructions that arrive by email without calling to confirm. When it is done, the keys are yours.

A few honest expectations

The roadmap is clean, but real deals have texture. An appraisal can come in low. An inspection can send you back to the negotiating table. A loan condition can pop up in the final week. None of these mean the deal is broken. They mean it is a normal transaction, and they are exactly the moments a good agent earns their keep. For genuinely legal questions, lean on the title company or an attorney, and for tax questions, a CPA. My job is to keep it moving and make sure you understand the step you are standing on.

Buying a home does not have to feel like a leap into the dark. When you know the order of the steps and have the right people walking them with you, the nerves give way to momentum. If you are thinking about a move in West Michigan, reach out and I will help you line up a lender, map out your search, and walk you through every step to the keys.